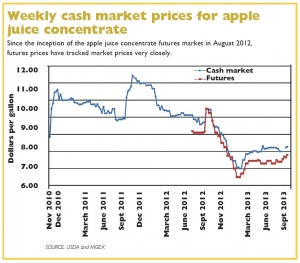

Weekly cash market prices for apple juice concentrate for 2012.

Kevin Barley

Apple growers might one day be able to get more money for their cull apples by making use of the Apple Juice Concentrate Futures Market that began operation a year ago last August.

They can use the market right now if they want to—anybody can buy or sell futures contracts—but it would be speculative. Many farmers who grow commodities like corn or soybeans sell contracts for future delivery as a hedge should cash prices decline. In theory, apple growers could put a floor under the price of juice- grade apples.

As it stands today, however, apple growers are a bit removed from the final product. As an analogy, imagine a wheat grower having to buy futures contracts for loaves of bread. Sometimes, the price of wheat and bread seem barely related, and that can be true of apples and apple juice concentrate as well.

Nonetheless, the apple juice concentrate futures market could be made to work for growers, according to Kevin Barley, a futures specialist with Morgan Stanley in Orlando, Florida. Barley chaired the Juice Products Association committee that spent several years developing the apple juice concentrate futures contract, which began trading on the Minnesota Grain Exchange (MGEX) in August of 2012.

Barley is working now to educate key players in the market—those who buy apple juice concentrate, the processors who make it, and the packers who sort out the apples they sell to the processors as juice-grade apples.

It would help growers, he said, if the packers that buy their apples would use the futures market to put a floor under the price of apples they sell to processors who make apple juice, and the processors would use the market to reduce price risk with companies that buy juice for sale in the retail market.

Packers could offer forward contracts to growers, much as grain elevators now do for grain growers. Elevators offer the price for future delivery and then offset their risk in the futures market. “For a packer to offer a fixed price to the grower, he’d have to use futures,” Barley said. Otherwise, the packer would face the risk that the product value would decline while the pay price did not.

Several of Barley’s instructional seminars, and other information explaining the concepts around trading in apple juice concentrate, appear on the MGEX Web site (www.mgex.com) on the apple juice concentrate page.

Apple growers, even if they don’t use the futures market, can find good information on that Web site about stocks of apple juice concentrate, historical and current cash prices for processing apples, and fact sheets about apple juice concentrate and they can sign up for e-mail notices about the concentrate market.

Why futures?

The basic contract is for 1,800 gallons of 70˚ Brix apple juice concentrate. Concentrate has been trading around $8 a gallon, so the value of a contract is more than $14,000 and requires about 10 percent to be held as margin money.

There are several important elements that make the apple juice concentrate business risky and therefore make futures contracts valuable.

First, a key element for Americans is that most apple juice concentrate is not made in America; it is made in China, Poland, and Argentina. Americans who buy concentrate have less than perfect information about what these concentrate makers are doing and will do, which puts them at risk between the time they buy the product and when they sell it.

There is uncertainty all along the chain from grower to retailer. Futures contracts can reduce that uncertainty. “As the futures market catches on, it can change the way the entire industry operates,” Barley said. “But it’s an educational process.”

A second element is the low value of cull apples. “Growers don’t really care about the price of juice apples,” Barley said. “It’s like pennies to them compared to the price of fresh-market apples.”

Even under the best circumstances, the value of juice apples to the grower would be about half of the wholesale value of the juice, with the other half going to the processor. A ton of apples will make about 27 gallons of concentrate, Barley said, which at $8 a gallon is worth $216 to the processor. Juice apple prices typically range widely from about $65 to $150 a ton, less when there’s a glut, more when they’re scarce.

Before working on apple juice concentrate, Barley spent years perfecting futures contract trading in orange juice. That’s different, he said, because, unlike apples, most oranges he is dealing with are grown for their juice and are not a byproduct of the fresh market. •

Leave A Comment