A new Washington State University economic analysis of planting Concord or wine grapes, shows that juice grapes may not be a wise investment right now, although wine grapes show a positive cash flow.

Dr. Raymond Folwell, WSU economist, told growers attending the annual meeting of the Washington State Grape Society that it appears the low price cycle for juice grapes, which typically lasts about ten years, may be starting to trend upward. But, even with higher grower returns, he said it would be difficult today for a new Concord vineyard to break even.

The booming years of high Concord prices in the late 1980s and again in the late 1990s were brought on in part by demand for the sparkling wine Cold Duck, crop failures in other areas, and publicity about health benefits. Washington State, with 25,000 acres and average annual production above 200,000 tons, is the leading producer of Concords and will likely continue to be, Folwell said.

"But don’t expect acreage to grow," he said, adding that competition comes from eastern production areas, California grape concentrate, and imported concentrate. Most imported concentrate now comes from Argentina.

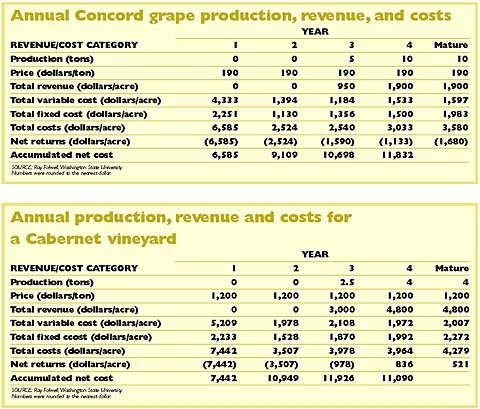

To determine the viability of establishing a Concord vineyard, Folwell used several different methods. He updated WSU’s Concord grape enterprise budget, basing the budget on the costs and receipts of planting and establishing a new 50-acre vineyard.

In the enterprise budget, he assumed a four-year establishment period, vines spaced seven by nine feet apart, and an average yield in year four of ten tons per acre. Enterprise budgets are developed with the new operator in mind, not established growers who already have land and equipment.

"The enterprise budget is an estimation of costs—custom pruning, custom harvesting, a management fee, and more," he explained, adding that it also includes new equipment. "It contains all the fixed costs and some that people don’t like to recognize."

Under the enterprise budget scenario, the accumulated net cost of establishing the vineyard through the fourth year was $11,830 per acre. Even when the vineyard matured, with prices averaging $190 per ton for grapes, net returns were in the red at -$1,680 per acre.

He then adjusted the numbers to compare breakeven prices necessary to cover costs. A grower averaging ten tons per acre would have to receive $358 per ton to cover his or her costs. Folwell estimated cash prices of Concord grapes in 2006 to be around $135 per ton. Folwell took his calculations a step further, developing a cash-flow statement for years one through ten. The cash flow includes operating activities, investing activities, and financing activities (establishment, equipment, and principal debt). "As you look at the numbers in years one through five, the cash flow is negative. But in years six and seven, it’s still negative. It’s not until year eight that you see a positive cash flow.

"Is it a good investment?" he asked. "Not today. It would take more than ten years to pay back the internal rate of return."

A cost-of-production calculator, under development through the Washington Wine Industry Foundation, will soon be available on-line to help wine and juice grape growers in calculating production costs. On-line calculators, which have already been developed for tree fruit growers, enable growers to analyze their own costs of production and breakeven prices and to assess the impact of production changes.

Wine grapes

The economic scenario is much brighter in Washington for wine grapes.

Despite a worldwide oversupply of wine grapes, the Washington wine industry continues to expand. Statewide production in 2006 was 9 percent higher than the previous year at about 120,000 tons, with more than 475 bonded wineries in existence. The fastest growing and most profitable U.S. wine market is the premium wine category ($7 or more per 750- ml bottle), which bodes well for the state’s wine industry which has targeted premium wines as its niche.

Folwell used the same economic analysis for wine grapes as for Concords, although the Cabernet Sauvignon vineyard was 55 acres and vines were planted on a six- by nine-foot spacing. He based his vineyard costs on standard viticultural practices, installing drip irrigation and wind machines.

Under the budget enterprise estimation, total establishment costs through year four were $11,090, slightly higher than establishment costs for juice grapes. But by year four, the vineyard had its first positive net return of $835 per acre.

He also looked at wine grape establishment costs under the cash-flow statement scenario, as he did in Concord grapes. "By the third year, a positive cash flow of $500 per acre begins and continues through to year ten, reaching almost $1,800 per acre by year nine."

Growers could reduce some of the expenses associated with the first-year establishment costs, he noted, like not installing the trellising or wind machine until the second year, or trying to grow a small crop in the second year. But he warned that in doing so, growers set themselves up for higher production risks.

Leave A Comment